It turns out the "Great Resignation" is more of a "Great Reckoning," according to a survey by consulting firm Mercer.

In other words, the movement is more about who is quitting their jobs rather than the sheer number of people doing it.

To be sure, Americans are leaving their employers in record numbers, with 4.4 million saying "I quit" in September alone.

More from Invest in You:

The 'Great Resignation' is burning out those who stay

Suze Orman: Can you afford to join the Great Resignation?

Is a 4-day workweek the answer to employee burnout?

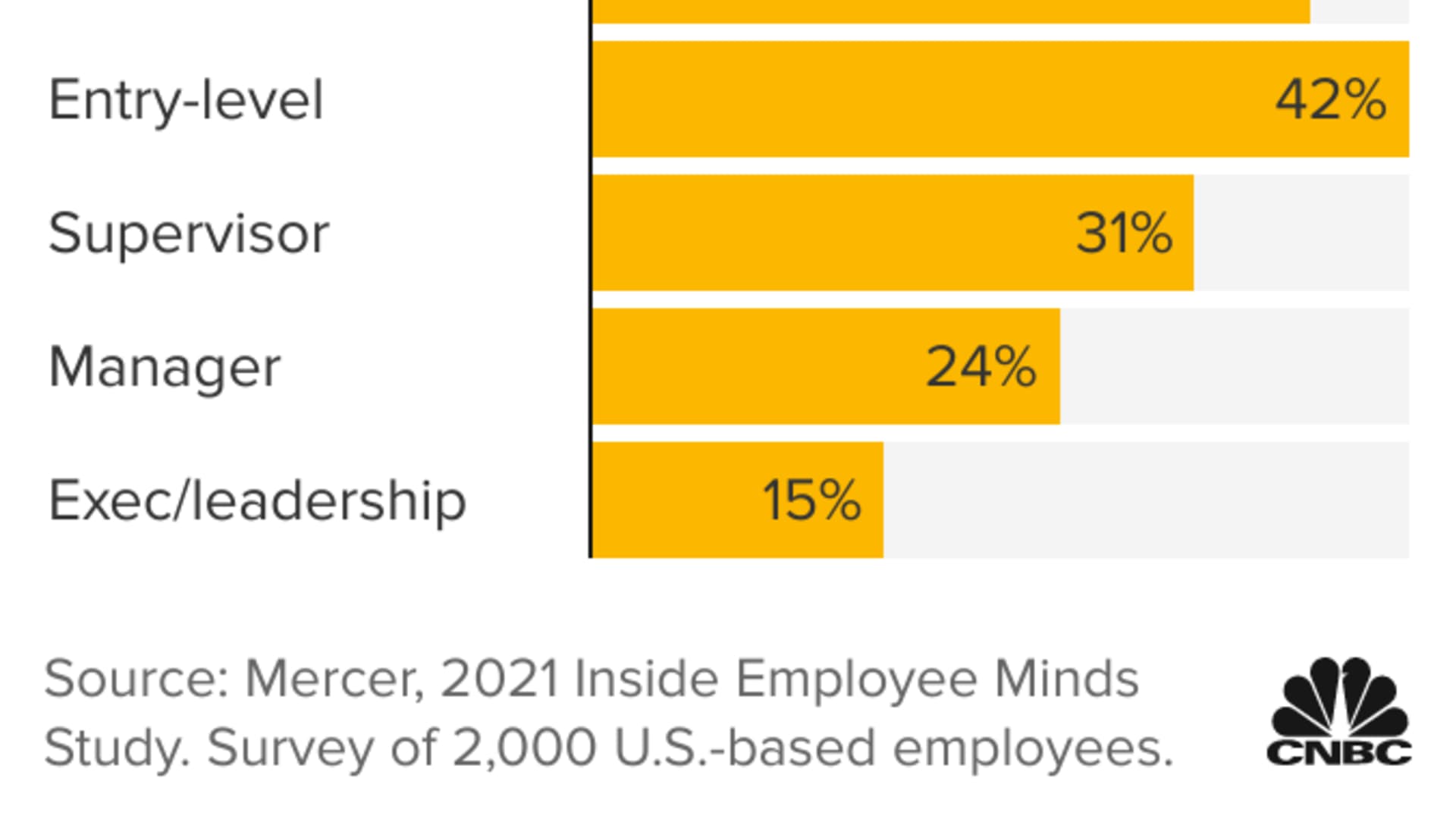

Yet, Mercer found that only 28% of respondents said they were seriously considering leaving their current employer, which the firm said is consistent with historical patterns it has seen in its data.

It is the low-wage, frontline, minority and lower-level employees who are more likely to want to leave, at rates significantly higher than the norm, the survey found. Those who made less than $60,000 per year were classified as low-wage.

Get Tri-state area news delivered to your inbox.> Sign up for NBC New York's News Headlines newsletter.

Concerns about basic financial wellness, like being able to pay bills or get rid of debt, have long weighed on low-wage workers, said Melissa Swift, Mercer's U.S. transformation leader.

"That's been a psychological stressor forever," she said.

Money Report

"Then we finally hit the point with many psychological stressors during the pandemic that that group has said, 'You know what, my options are changing. I don't need to live under this cloud forever.'"

Those choices include higher wages and the option to work remotely.

For Stephanye Blakely, 36, the decision to quit her job during the pandemic was an easy one. A single mother living in Louisville, Kentucky, Blakely was working the overnight shift sorting packages for a delivery company. When her 7-year-old son's school shut down and shifted to virtual learning last year, something had to give.

"For me, it was kind of a wake up call and a way of reassessing where I was and where I wanted to be," Blakely said.

She eventually enrolled in a coding boot camp with Hack Reactor and is now a software engineer — working remotely. She went from making $14 an hour to more than $40 per hour, she said.

"Two years ago, I wasn't thinking too much about how I'm going to save up for college for my son because we were worried about what we were going to be eating," Blakely said.

Now, she's looking to buy a house.

"There's money going into savings," she said. "I'm able to do investing."

What employers should do

To attract and retain workers, employers should embrace flexibility, address burnout and create a safe space for Black employees, Mercer's report concludes.

They should also prioritize hourly, front-line and low-wage workforces. Pay is a big issue, as are employer benefits.

"Some of our research suggests employers are saying they can't get the talent they need, but workers are saying, 'I'm not paid enough for the skills I have,'" Swift said.

"So there's a change in that mental calculus of what is the skill actually worth in the market and just resetting that."

Employers should also look at how they have set up work fundamentally.

"A lot of it has to do with banal things, like how shifts are set up, how people get assigned to shifts, what their tasks look like, how they're managed, doing those tasks," Swift said.

"It makes a huge difference as to whether or not people actually enjoy their jobs and want to stay at them."

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: 'It was the worst financial decision': 3 money experts on their biggest spending mistakes with Acorns+CNBC

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.