Utah homeowner Katherine Cwik says she panicked after she found out she owed a lump sum of nearly $4,700 on her mortgage — far more than the three months of mortgage payments she thought she deferred back in March.

Cwik, 55, who works in the airline industry, applied for a deferral of her mortgage payments on March 20, after she agreed to take an unpaid leave as part of her company's plan to free up payrolls. She's been able to collect unemployment and is supposed to return to work in August.

But with the future of her job uncertain, Cwik wanted to shore up her finances. She thought applying for a mortgage deferment would allow her to build a savings cushion. Cwik owns a townhouse in Salt Lake City and pre-pandemic paid roughly $900 a month for her mortgage, which includes her principal, interest and escrow.

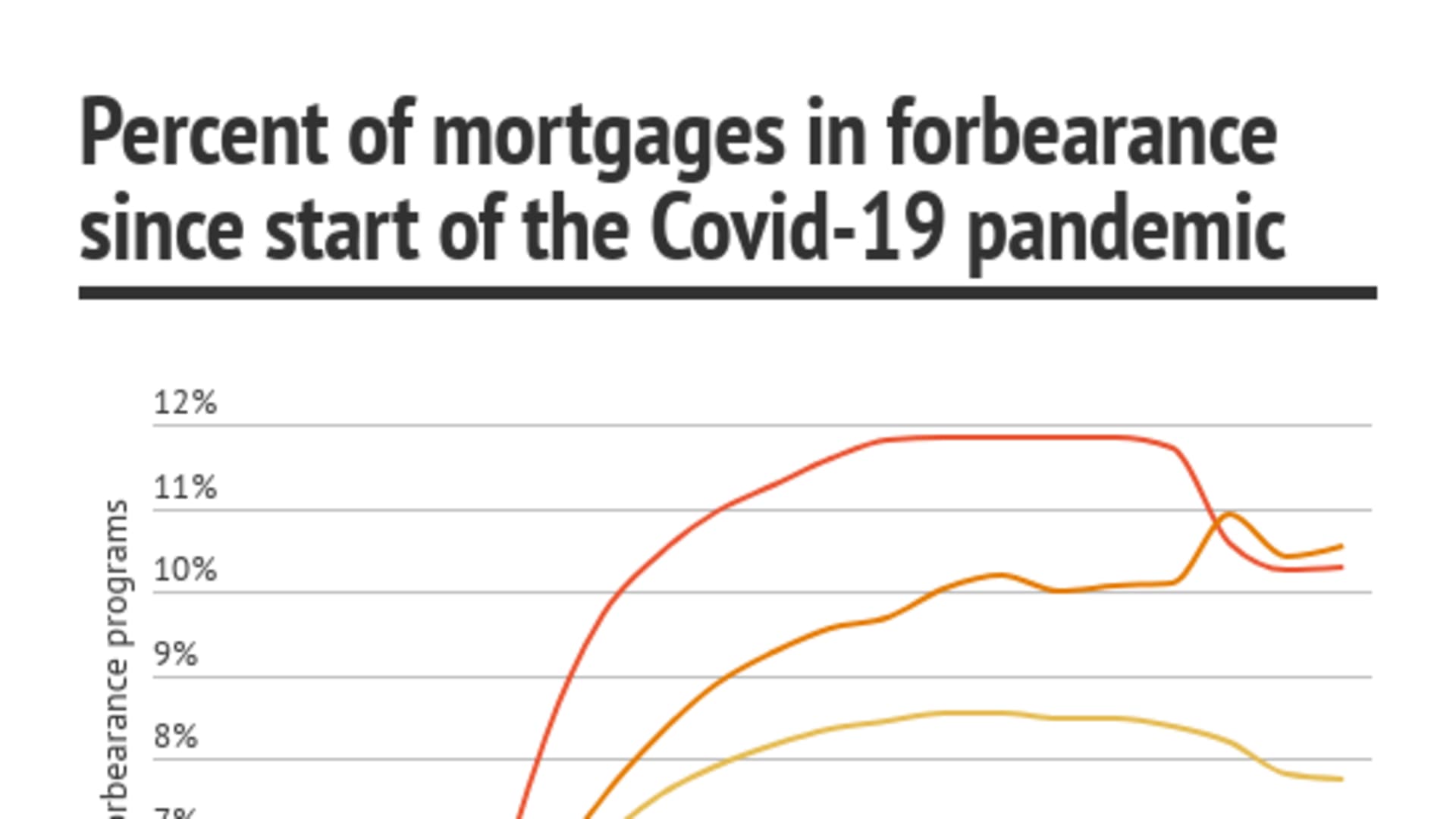

About 3.9 million U.S. homeowners are currently in forbearance, according to the latest estimates from the Mortgage Bankers Association. Forbearance programs generally imply that homeowners can suspend mortgage payments for a time and then repay the outstanding balance in a lump sum when they resume their normal bill cycle. Deferment programs typically allow homeowners to push payment of any missed payments to the end of the mortgage period.

In March, in response to the coronavirus pandemic, the federal government and many financial institutions launched mortgage relief programs. But five months later, consumers are still struggling to understand the terms surrounding the assistance and many feel banks are failing to help their customers navigate the process.

Cwik's five-month journey through the mortgage relief process is emblematic of many of the issues that consumers are facing: long wait times to connect with the mortgage servicer, unfamiliar terminology, vague answers from customer service and, at times, incorrect information.

In March, Cwik says she spoke with a customer service rep at Bank of America, which handles her mortgage. She was left with the understanding that she was eligible for a three-month deferral program and that any missed payments would be added to the end of her 30-year mortgage. After three months, Cwik says she believed she could start making payments again or call back for more assistance.

Money Report

"I cried when I got off the phone because I thought, Oh, my God, this is great and that's a real relief for me right now," Cwik says.

But as it turns out, the relief was short-lived.

What happened when payments restarted

Three months after Cwik received mortgage relief, she sent in her normal payment of roughly $900 — plus a little extra since she likes to overpay when she can, $5 this time — for her July mortgage payment.

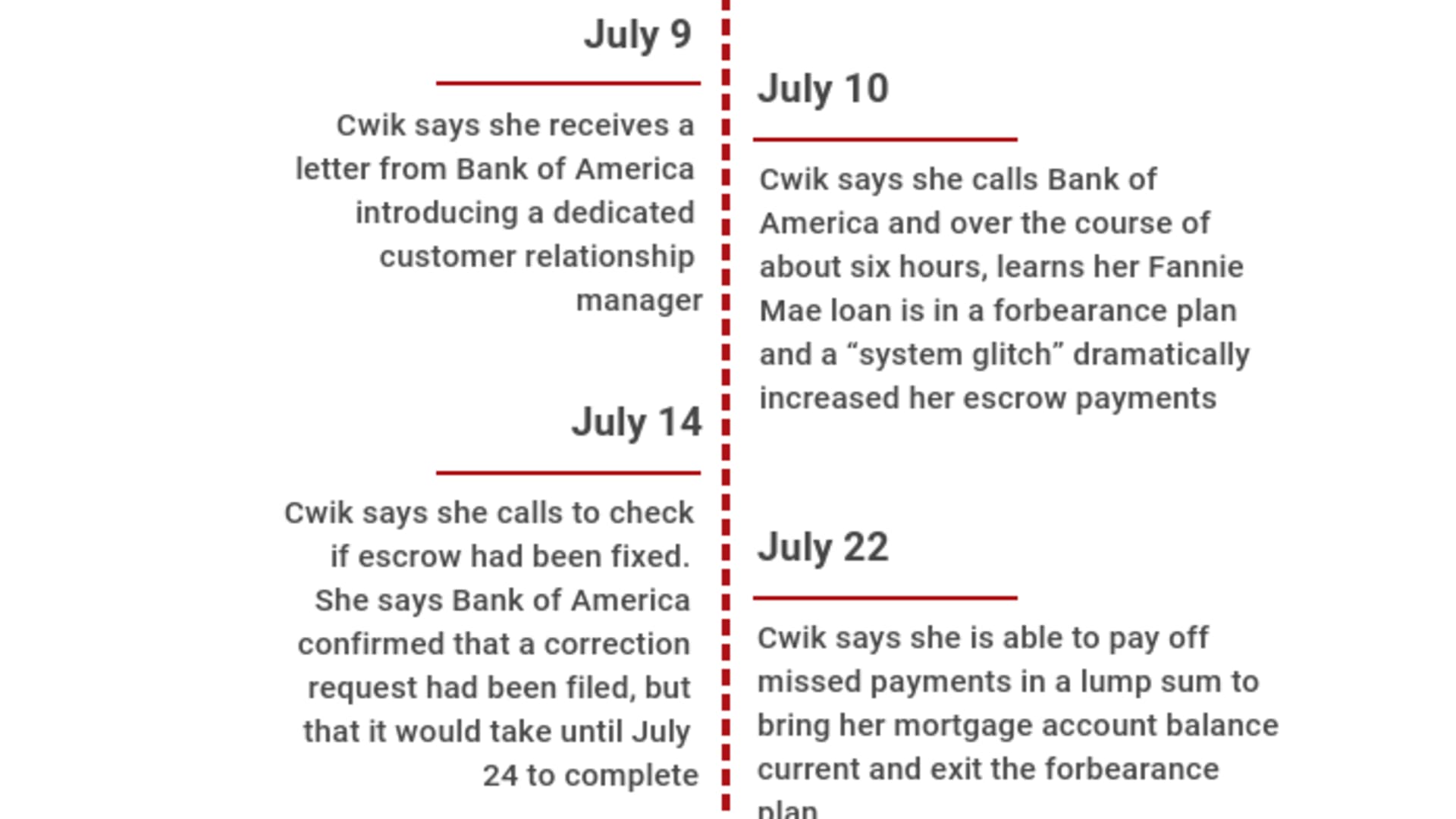

On July 9, she received a letter from Bank of America introducing her to a dedicated customer relationship manager and asking her to please call. When she called the bank, she was in for a shock: The home retention department staff told her she owed $4,693 on her mortgage immediately.

"I about fell over," Cwik says. "I'm thinking, how does that even compute? I got the relief for three payments. That's $3,000. Where is this number coming from?"

But the representative didn't have any answers. Instead, she set up an appointment so Cwik could talk with her customer relationship manager the following day. But when the case manager didn't call, Cwik decided to take matters into her own hands and call the bank the next day.

Cwik says that kicked off a six-hour odyssey, with her calls being bounced between several different departments as she fought to get to the bottom of the issue. Several of the Bank of America customer service representatives kept talking about Cwik's enrollment in a forbearance program. "I said, That's not what I signed up for. And I kept saying that because I wanted to be sure if it was being recorded, that it was on the record," she says.

Turns out, that's exactly what she was signed up for. Bank of America announced in mid-March it would offer payment relief programs, including deferment and forbearance programs for mortgages held by its customers. But Cwik learned in July that she has a Fannie Mae loan that is serviced by Bank of America, not owned by the bank. That wasn't clear on her initial call, Cwik says.

Because Cwik applied for mortgage assistance programs before the CARES Act passed and solidified many of the relief programs for federally-backed loans, she wasn't eligible for deferment. In fact, Fannie Mae didn't even have a true deferment option at the time, only a forbearance plan that required customers to pay back missed payments in a lump sum.

"I was on the phone for almost six hours. I can't imagine how many people don't have six hours to spend," Cwik says.

While Bank of America first rolled out its mortgage relief programs in the early weeks of the coronavirus pandemic, the bank said in a statement to CNBC Make It that it is continuing to offer mortgage assistance options to help clients who need it, including those who have mortgages owned by government-sponsored enterprises (like Fannie Mae). Bank of America says it has deferred approximately 200,000 mortgages during the pandemic.

Bank of America blames 'system glitch'

But even if Cwik's mortgage was in forbearance, it still didn't explain why her repayment was almost $2,000 more than she expected. One Bank of America rep told her that she could now apply for a deferral, but after the program ended, her monthly payment would be approximately $1,610 a month.

"I said, Wait a minute. That's almost double my mortgage payment," Cwik says. "So you're telling me I have to pay that until the end of my mortgage? I still have about 20 years left. That's $180,000. That's more than my original loan. My original loan was for like $132,000."

She spoke with five people at BoA before someone figured out the issue: Her escrow payment was exponentially larger now than when she went into the forbearance program.

The amount due to escrow can fluctuate year to year, as lenders typically recalculate escrow payments on an annual basis and may take into account increases in your homeowner's insurance premium or rising property taxes. But Bank of America had already completed its annual review of Cwik's account earlier in the year and actually reduced her minimum monthly mortgage payment, including escrow, from $900 to just under $850. So she was confused why it would increase after forbearance.

After getting transferred yet again, Cwik says a rep in Bank of America's escrow department told her that a "system glitch" was behind the issue of her increased payment amounts. He said it would take 24 to 48 hours to fix the problem.

Because the update was going to take a few days to process, Cwik says she agreed to be placed in another forbearance plan so she would not be considered delinquent and rack up fees. "I wanted to be sure the escrow debacle was handled first — and then see what I actually owed," she says.

To repay her missed mortgage payments, Cwik says the representative gave her several options, including paying the balance back over the course of six months, applying for a loan modification or paying a lump sum.

"I just wonder how many Bank of America mortgage customers have experienced the escrow 'system glitch' and are in grave fear of how they are going to pay a lump sum, or even a larger mortgage for six months, to pay off the one to three months of payment relief they thought they had," Cwik says.

Bank of America did not specifically respond to CNBC's request for comment regarding the system glitch.

The return to normal

After all those hours on the phone, Cwik's mortgage payment situation still wasn't completely solved. She was initially told it would take until July 14 to fix the "system glitch," but when she called back on that day to double check, she says Bank of America confirmed that a correction request had been filed, but that it would take another 10 days to complete.

In the meantime, Cwik says she received paperwork in the mail from Bank of America saying: "We're pleased to let you know that you've been approved for our Coronavirus Payment Deferral Program" — an option Cwik says she did not want to take at that point and did not sign up for. Additionally, Cwik says she received conflicting information on what her exact mortgage payments would be going forward while the correction request was being processed.

Cwik finally reached a resolution with her mortgage issues about two weeks after she initially contacted Bank of America in early July. Cwik says she called to check on the status of the correction request on July 22 — spending another couple of hours talking with a helpful customer service rep she'd previously worked with.

In the end, Cwik agreed to pay a lump sum to bring her mortgage account current. Because Cwik typically pays a bit more on her mortgage than is required, she had an over-payment balance of roughly $1,040 on her account (including the extra $5 she paid in July), which she could apply to her outstanding mortgage payments. She says the customer service rep told her she would have to pay an additional $1,497 to make her account current. All told, Cwik estimates the outstanding balance was about $2,537, which is roughly the equivalent of three monthly mortgage payments before she went into forbearance.

After making the lump-sum payment, Cwik opted to cancel the additional three-month mortgage relief program she says she agreed to be placed into earlier in the month. "I'm just a normal BofA mortgage account customer now," Cwik says, but adds that she's still concerned about the homeowners who don't have the time, energy and fortitude to keep calling to make things right.

"We have worked with the client and have resolved her issues," Bank of America said in a statement to CNBC Make It. When CNBC reached out the bank for comment, Bank of America requested Cwik's name and location, and Cwik agreed to let CNBC share it. She tells CNBC she received a voicemail from the bank's executive mortgage complaint team several hours after her name was provided to Bank of America.

Going forward, Cwik's monthly mortgage will be $846, which is slightly lower than the amount Cwik was set to pay after receiving her escrow review earlier in the year.

But in the end, Bank of America's relief program, and the process, didn't help her build much of a savings cushion as she had planned, Cwik says. "In fact, I paid extra if you consider the amount of time I have spent trying to make everything in proper order," she says.

Given the choice, would she do it again? Absolutely not, Cwik says. "I have little trust in the company that is the public face of my Fannie Mae mortgage loan."

If you have experienced issues with mortgage relief, we would like to hear from you. Please email senior money reporter Megan Leonhardt at megan.leonhardt@nbcuni.com

Check out: The best credit cards of 2021 could earn you over $1,000 in 5 years